What I’m reading in the news regarding the housing market

Boston Condos for Sale

What I’m reading in the news regarding the housing market

If you’ve been holding off on buying a Boston condo because of high mortgage rates, you might want to take another look at the market. That’s because mortgage rates have been trending down lately – and that gives you a chance to jump back in the Boston condo for sale market.

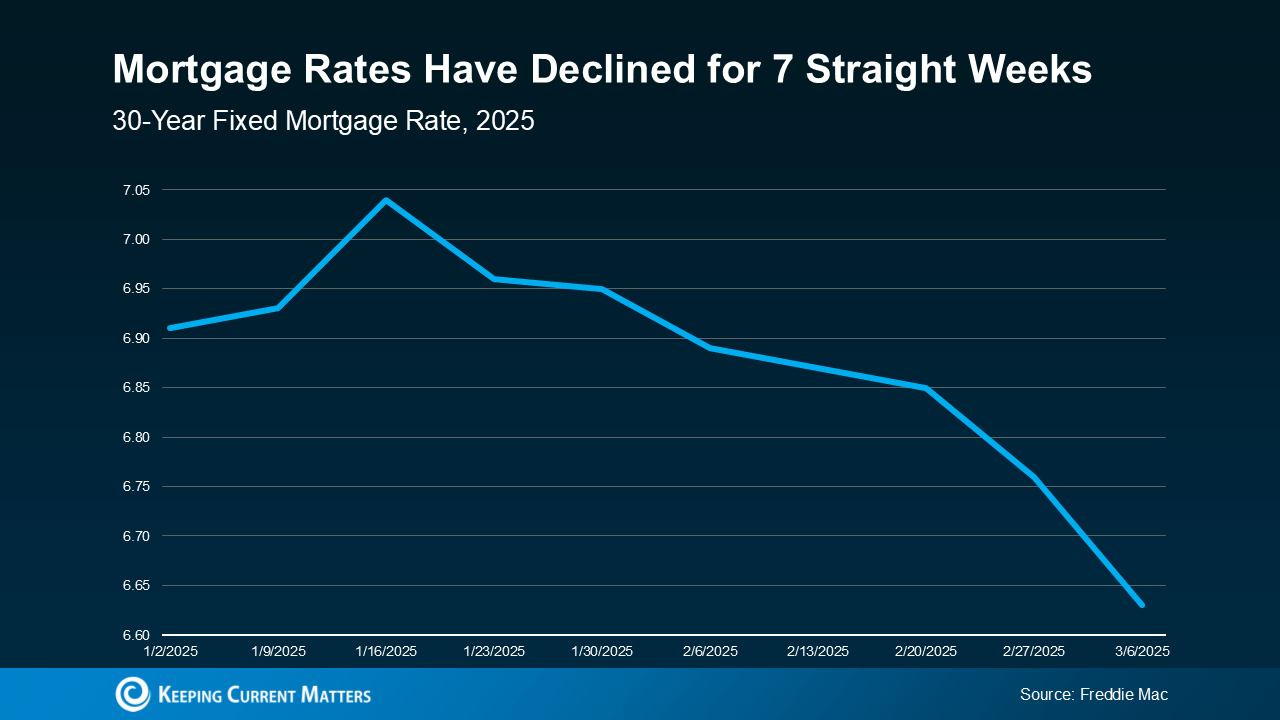

Mortgage rates have been declining for seven straight weeks now, according to data from Freddie Mac. And the average weekly rate is now at the lowest level so far this year (see graph below):

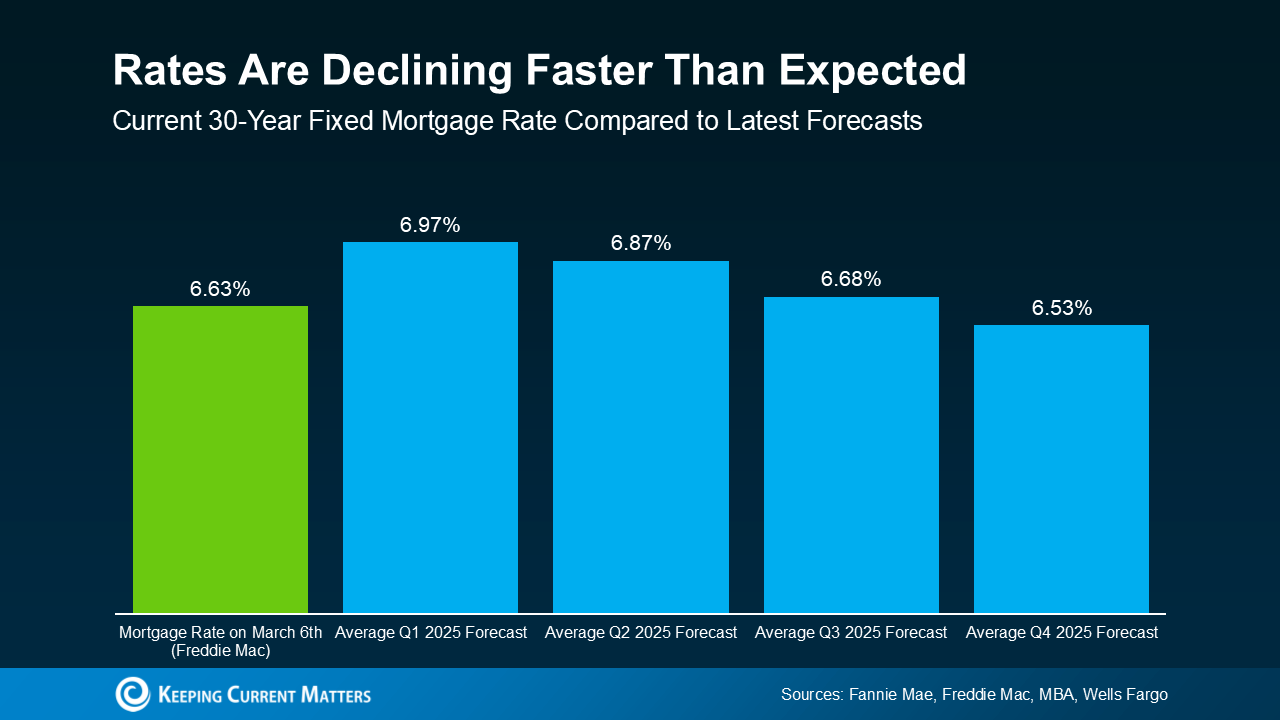

While that may not sound like a significant shift, it is noteworthy. Because the meaningful drop from over 7% to the mid-6’s can change your mindset when it comes to buying a Back Bay or Seaport condo. Especially when the forecasts said we wouldn’t hit this number until roughly Q3 of this year (see graph below):

While that may not sound like a significant shift, it is noteworthy. Because the meaningful drop from over 7% to the mid-6’s can change your mindset when it comes to buying a Back Bay or Seaport condo. Especially when the forecasts said we wouldn’t hit this number until roughly Q3 of this year (see graph below):

Why Are Boston condo Rates Coming Down?

According to Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), recent economic uncertainty is playing a role in pushing rates lower:

“Mortgage rates declined last week on souring consumer sentiment regarding the economy and increasing uncertainty over the impact of new tariffs levied on imported goods into the U.S. Those factors resulted in the largest weekly decline in the 30-year fixed rate since November 2024.”

And the timing of this recent decline is great because it gives you a little bit of relief going into the Boston condo for sale spring market. Just remember, mortgage rates can be a quickly moving target, so you should expect some volatility going forward. But the window you have as they’re coming down right now might be the sweet spot for your purchasing power now.

What Lower Rates Mean for You as a Boston Condo Buyer

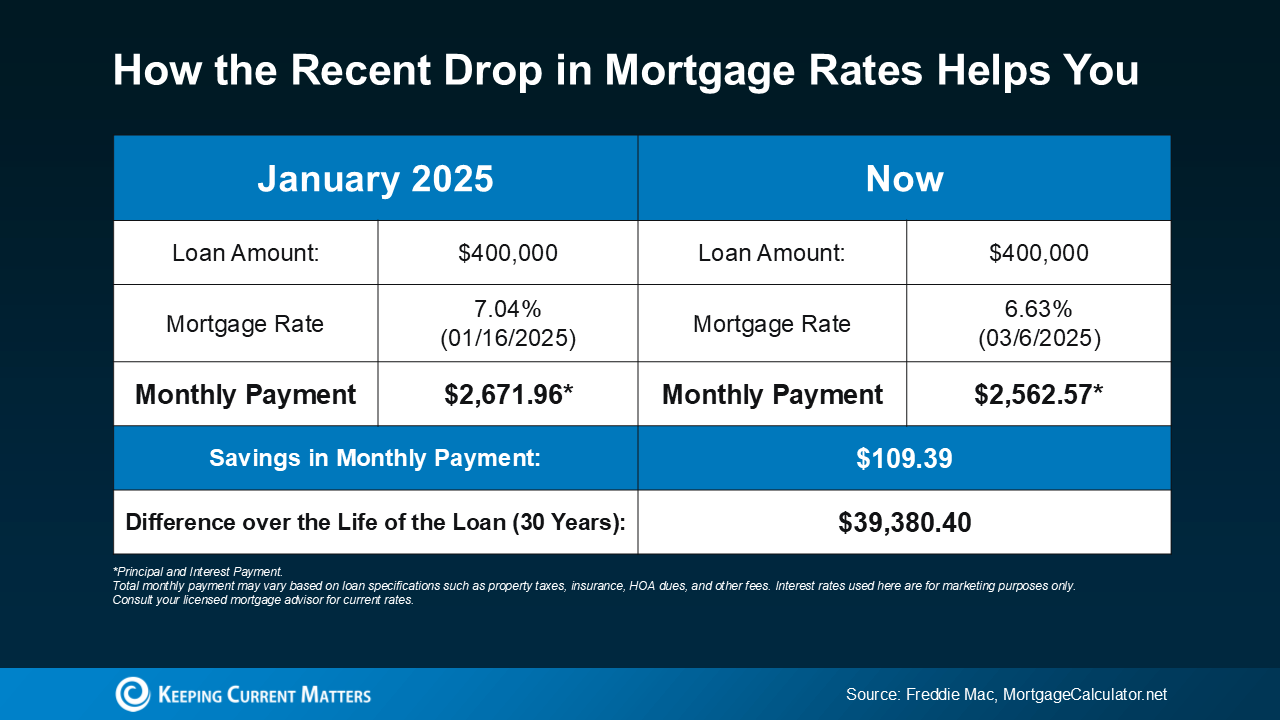

Even small changes in rates can make a difference to your monthly Boston condo payment. Here’s how the math shakes out. The chart below shows what a monthly payment (principal and interest) would look like on a $400K home loan if you purchased a condominium when rates were 7.04% back in mid-January (this year’s mortgage rate high), versus what it could look like if you buy a home now (see below):

In just a matter of weeks, the anticipated payment on a $400K loan has come down by over $100 per month. That’s a significant savings. When you’re making a decision as big as buying a home, every bit counts.

In just a matter of weeks, the anticipated payment on a $400K loan has come down by over $100 per month. That’s a significant savings. When you’re making a decision as big as buying a home, every bit counts.

Just remember, shifts in the economy drove rates down faster than expected. But that can change, making rates volatile in the days and months ahead. So, if you’re waiting for rates to fall further before you buy, think hard about the current window of opportunity if you’re ready to act.

Boston Condos and the Bottom Line

Mortgage rates have dipped, giving buyers a bit more immediate breathing room. If you’ve been waiting for rates to ease before jumping in, this could be your window.

____________________________________________________________________________________________

What I’m reading in the news regarding the housing market

Lawrence Yun, National Association of Realtors chief economist, joins ‘Power Lunch’ to discuss what spurred the recent decline in housing data, what a rise in listings tells Yun and more.

Click Here to view: Google Ford Realty Inc Reviews

Updated: Boston Real Estate Blog 2025

————————————————————————————————————————————————————————

Throughout the pandemic, demand for housing towered over the supply of new and existing homes and caused prices to mushroom as the seller’s market only intensified. However, while the market is still smoldering hot, there are some indications and predictions that the pace may begin waning in the coming months.

In June, the median sale price of an existing home hit a record high of $363,300, according to the National Association of Realtors. That marks a whopping 23.4% increase from June 2020, when the median sale price hovered at $294,000. But will prices keep inflating? The NAR’s housing and commercial research director, Gay Cororaton, said yes, but at a slower pace.

Several factors are driving the surges, but supply and demand lead the list, according to Cororaton.

Inventory was already tight before the pandemic began, a trend that started in 2012, according to Cororaton. She said that one constraint was labor supply, affecting the housing market even before COVID-19 began wreaking havoc on the economy. Various zoning regulations were also not conducive to increasing supply, she added.

“Even before the pandemic hit, supply was already tight. Then the pandemic comes around, people don’t want to list their homes, and then the supply-chain issues affecting lumber and … appliances,” Cororaton said. “All of those just came together, causing this more critical supply issue.”

Cororaton said that there has recently been some easing in demand for homes and a bit of an uptick in supply. She said that the U.S. had just about 1.9 months’ worth of supply for existing home sales at the beginning of the year. At the end of June, the inventory of homes for sale was 1.25 million, a 2.6-month supply at the current sales pace. The month prior, there was a 2.5-month supply.

“It’s still being driven by low mortgage rates,” she said, pointing out that they did tick up slightly but are essentially flat. She said those low mortgage rates are fueling the demand but said that inventory is still tight.

Cororaton noted that while housing prices are up some 23% year over year, wage growth has not kept pace with those breakneck increases, meaning that it could potentially be more difficult for people to purchase homes now than a year ago.

Cororaton predicted that the U.S. will begin experiencing slower demand but said that she thinks inventory will remain tight, which means prices won’t start falling in level terms as the country approaches next year.

She said that because of that supply tightness, her group is not forecasting the level of prices will go down but rather thinks that there will be a slowing in the pace of growth.

“The pace of appreciation is going to slow to less than 5%. We won’t see double-digit price inflation,” she said, “but we won’t see this broad-based decline in prices.”

Patrick Gourley, an assistant professor of economics at the University of New Haven, told the Washington Examiner that in the spring of 2020, there began to be a deluge of people wanting to move out from urban areas and have suburban single-family homes in light of the COVID-19 pandemic.

“That paired with the lack of people wanting to sell their homes really kind of seized up the housing market,” he said, noting that some parts of the country saw even more profound spikes in housing costs than others.

Gourley said that for the health of the U.S. economy, he hopes that the country is starting to see the housing market begin to cool off, but he said that in the near future, at best, he thinks there is a chance it could be plateauing.

“It’s not so much it’s cooling, as it’s just staying the same,” he said of the market. “I don’t know if there is much evidence that we’ve seen a peak yet.”

He said that if prices plateau, it’s a neutral conundrum because it means that the housing market isn’t getting worse, but it also isn’t getting any better for those who want to go out and purchase a home.

But should people go out and try to buy a house now? Gourley said that many people, especially those younger and who might not have the means to purchase a home, now have decided to wait and see what the future holds.

Apart from supply and demand, Cororaton did say there might be some slight cooling in the fall compared to the summer, which she attributed to seasonal factors that happen each year and not necessarily concrete changes.

Another factor in the housing market equation is inflation, which has become a noticeable side effect of U.S. economic recovery. Inflationary pressures have consistently outpaced expectations from the Federal Reserve and other economic forecasters, including those in the Biden administration.

According to the most recent report from the Department of Labor, consumer prices increased 5.4% in the year ending in July. The figure was slightly higher than expectations but was less dramatic than the lurching price increases seen over the previous few months.

The Federal Reserve has not veered from its pandemic-era monetary policies to slow inflation but has rather decided to keep interest rates near zero. The central bank has said it won’t hike rates until inflation runs at 2% and there is full employment. The Fed has acknowledged that inflation has been higher than expected but claims that it is transitory and that prices will fall.

Cororaton highlighted the two indicators that the Fed examines regarding interest rate changes, inflation and unemployment, and said that she thinks, given the economy’s trajectory, the central bank might start raising rates a bit as soon as the middle of next year.

“So, I think in terms of whether you want to wait for prices to fall — they’re not going to fall — and you will only see interest rates ticking up. So, if you have the down payment now, lock in that low mortgage rate now,” she said.

All in all, the housing market is largely in wait-and-see mode. Although the pace of housing-price increases might end up slowing, it isn’t easy to project out exactly what may happen.

“There’s obviously a crystal ball aspect to this. Who knows what’s going to happen in the coming weeks, let alone months or years?” Gourley said.

Boston Condos for Sale

_____________________________________________________________________________________________________________________________________________________________________________________________________

What I’m reading in the news regarding the housing market

Recently, I’m reading more and more that some so-called experts think that we might be heading into a housing bubble, especially in the suburbs of downtown Boston.

What is a housing bubble?

Before we jump into our current situation, let’s first take a look at what a housing bubble actually is. Also known as a real estate bubble, a housing bubble occurs when home prices rise at a rapid rate to a level of instability. Housing bubbles generally begin when there is a shortage of inventory and an increase in demand in a market. As the prices start rising, speculation begins to take effect. Consumers expect prices to increase further, so everyone wants to buy a home as quickly as possible. This drives up demand further and prices continue to skyrocket.

As we know from physics, what goes up must come down. So at some point, the steep housing prices become unsustainable and homes become overvalued. When this happens, demand begins to decrease and therefore, supply starts to rise. Suddenly, we’re in a situation where there are more homes for sale than prospective buyers. As a result, housing prices can fall drastically – and the bubble bursts.

What leads to a housing bubble?

Bubbles are a phenomenon that can happen in just about any industry, whether it’s homes, stocks, or gold. Traditionally, bubbles don’t often occur in the housing market because of the large financial responsibility associated with purchasing a home. However, with the right combination of factors, a housing bubble can begin. Here are several situations and variables that can occur, drive up demand, and lead to a housing bubble.

- A rise in economic activity. When the economy is doing generally well, people have more disposable income to spend on housing.

- Low mortgage interest rates. This puts homeownership within reach for many hopeful homebuyers.

- Loose mortgage lending practices. This is a major factor that led to The Great Recession as many lenders offered home loans to homebuyers without regard for their ability to repay.

- New mortgage products. Specifically, those allowing the buyer to make low monthly payments. This can make the idea of homeownership appear more affordable than it actually is.

- A sudden increase in migration. For example, if a large group of homebuyers relocates from a certain area, this will increase demand and shrink supply driving prices up further.

- The time it takes to build a house. It generally takes a long time to build a new home which makes supply slow to respond to dramatic increases in demand.

- Speculative and risky behavior. This can lead to more property investors entering the market, along with homebuyers who can’t afford the homes they are purchasing.

Boston Real Estate and the Bottom Line

My thoughts I don’t see a major danger in the downtown Boston condo market, On the other hand, I think the Boston suburbs are approaching dangerous price points.

What are your thoughts?