Mortgage News Update

Condos for Sale and Apartments for Rent

Mortgage News Update

Mortgage News Update

Inflation and several other key sectors of the economy had pushed the Federal Reserve to hike rates at the fastest pace in decades. When it looked like the data might provide some relief, rates quickly moderated.

Strangely (or so it seemed at the time), the Fed was highly reluctant to read too much into several months of generally more palatable data. They said it was too soon to draw any conclusions other than “it’s a start.” With that, markets hesitated to push longer term rates any lower until the data made an even stronger case of that. Which is placing condo buyers in a tougher position to afford a Boston for sale.

Unfortunately, the data since then has made a case for rates to turn around and head right back up toward previous highs. February has been particularly brutal in that regard and today was just the latest example. In fact, today’s reports aren’t typically regarded as top tier motivations for rate movement, but the market is so defensive to begin with that it doesn’t take much of a bump to create a snowball of momentum.

The average 30yr fixed quote for a top tier scenario was around 6.75% on Friday and was up to 6.87% by Tuesday afternoon. More than a few lenders are already back to 7%.

https://www.mortgagenewsdaily.com/markets/mortgage-rates-02212023

___________________________________________________________________________________________________

Mortgage News Update

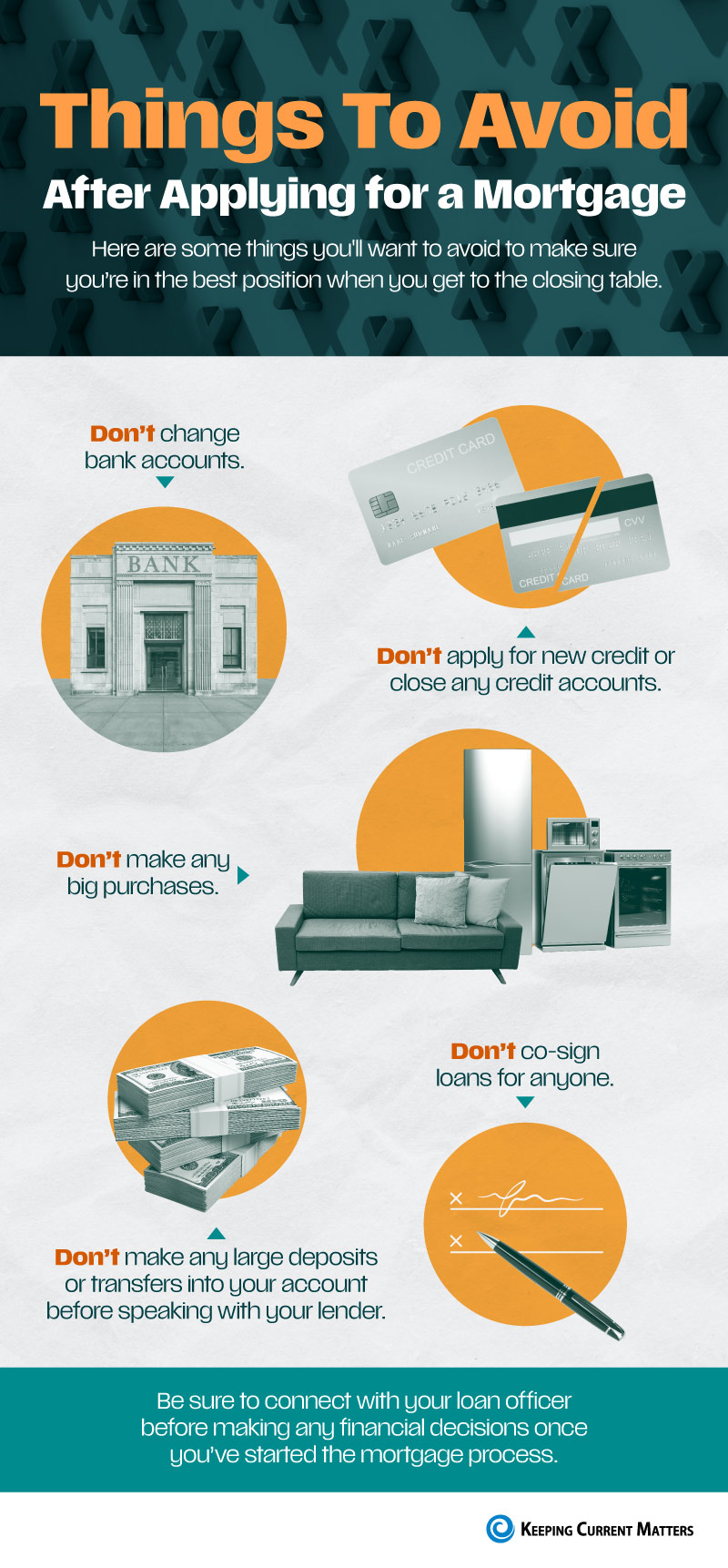

The Washington Post has an interesting article entitled: Applying for mortgage? Starting June 1, you could face another credit screening. Basically, the article states, if you’re thinking about applying for a home mortgage, beginning June 1, your lender is likely to order a second full credit screening immediately before your closing.

The reason: Mortgage lenders want to find out whether you have obtained — new debt between the date of your mortgage application and the closing.

If you’ve actually taken out new loans — let’s say furnishings for your new condo — that are sizable enough to affect the debt-to-income ratio calculations used in your original mortgage approval, the whole deal could fall through.

File Under: Once your mortgage is approved, hide your credit cards.