Boston Condos for Sale

Loading...

Boston real estate

One of our readers sent me an article about promoting a foreclosure scare due to the pandemic. I don’t see it. But it is worth noting because it could become a self-fulfilling prophecy just due to the lack of a counter-argument being published at large.

This article is quick to point out that there isn’t a problem yet:

What will happen when the foreclosure moratorium expires?

Even after the foreclosure moratorium expires, homeowners on a government-backed loan will have a forbearance option to fall back on, so there’s no need to panic just yet. But digging into mortgage-delinquency data shows how much water is building behind the dam that is these government backstops.

In January, just 3.22 percent of mortgages were in delinquency. By May, that number shot up to 7.76 percent — about three points shy of where the delinquency rate peaked during the financial crisis of 2008, which was at 10.57 percent.

It’s worth noting

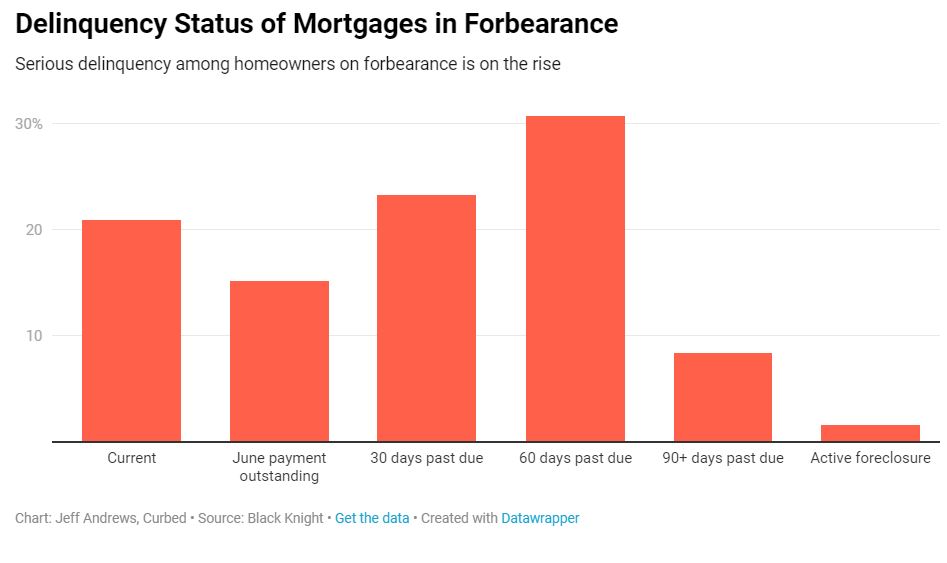

Prior to the pandemic in March, the number of mortgages in forbearance was fewer than 100,000. Currently, there are roughly 4.5 million mortgages in forbearance, although this is obviously a reflection of homeowners having the option of forbearance, it gives you a sense of the scope.

Not every homeowner in forbearance is past due on their payments; some went into forbearance as a precaution, or just because they could. Some homeowners were in forbearance and have since gotten out, either because there didn’t end up being a need or they got a new job. For June, 21 percent of mortgages in forbearance were current on their payments, but as the pandemic goes on, more will enter into serious delinquency that would normally trigger a foreclosure.

With the forbearance option available for up to a year, economists have baked into their models a wave of foreclosures in the spring of 2021, which they say would cause a very rare drop in U.S. home prices.

I haven’t heard anyone predict falling home prices in 2021, and Zillow is forecasting a 5.7% increase.

We also know that the loan-modifications that worked last time will get employed again before banks lose a penny. The only people they might foreclose on are homeowners with sufficient equity, but if it comes to that, then those folks will sell their house instead and make out nicely.

Boston Real Estate and the Bottom Line

It does add an interesting component to next year’s selling season though, which should be a humdinger!