Boston Downtown Condos for Sale and Rent

Over the years, Boston North End real estate has changed along with the people and the current and past styles. This video takes us back to an era long gone, but not forgotten. When viewing the video below take notice of the Boston North End buildings and apartments of the past era.

Compared to other parts of downtown Boston, one can still find Boston North End condos for sale for under $1,000 per square ft.

Click Here: Boston North End condo sales data

Boston North End Condos for Sale

Sorry we are experiencing system issues. Please try again.

Click Here: Boston Real Estate For Sale

Updated 2021

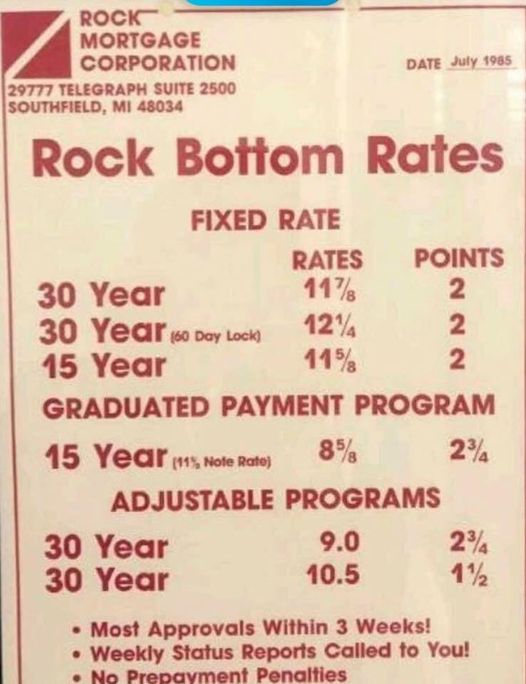

Mortgage rates July 1985

I had a conversation the other day in a Boston North End cafe and we were discussing the good old days when homes were cheap and everyone moved often. He is a mortgage originator, so I asked him how many adjustable loans he has done this year.

His answer? None.

Back in the day, adjustable-rate mortgages were the preferred product. Look at the difference:

$300,000 loan amount

Monthly payment at 11.875% = $3,057

Monthly payment at 9.0% = $2,414

Difference = $643 per month!

Nobody looked too hard at the terms of the ARM because a) $643 per month was a ton of money back then, and b) no one planned to stay forever. Home buyers could always refinance if they had to, but many solved their ARM concerns by moving again – heck, there were lots of homes for sale!

Then the 2-out-of-5-year tax exemption was passed in 1997 which really juiced the market. Homeowners were rewarded with tax-free money for moving!

It was rare that anyone had the full $500,000 in net profit, mostly due to the lower home prices and because of other recent moves. Yet many moved again just to say they got their tax-free money!

At the same time, the mortgage industry, led by Countrywide, flooded the market with an alternative – the interest-only mortgage with a rate that was fixed for the initial period, and you could choose 3, 5, 7 or 10 years. Once those saturated the market, Countrywide stole the neg-am ARM idea from the S&Ls and spiked them with high margins, and, well, we know how that ended.

As the private mortgage companies exited the market, the government lowered rates and backed Fannie/Freddie to provide market liquidity. For the last ten years, the only program being offered is the 30-year fixed-rate mortgage, and because rates are so much lower than before, buyers didn’t mind.

The end result? Today, you never hear anyone buying a home for the short term.

The combination of ultra-low rates and the difficulty of finding a better home has locked in everyone into their current home. Even if the current home becomes unsuitable, it beats moving again.

The low-inventory era is here to stay, and will likely get worse.